How to Buy a House With Bad Credit: What First-Time Buyers Need to Know

Many people assume that if their credit score is not perfect, buying a home is impossible. That is one of the most common misconceptions about homeownership.

While credit does play an important role in the mortgage process, having less than ideal credit does not automatically disqualify you from buying a home. Many buyers successfully purchase homes while they are still improving their credit.

The key is understanding what lenders look for and what steps you can take to strengthen your position before applying for a mortgage.

In this guide you will learn how buying a home with bad credit works and what options may still be available.

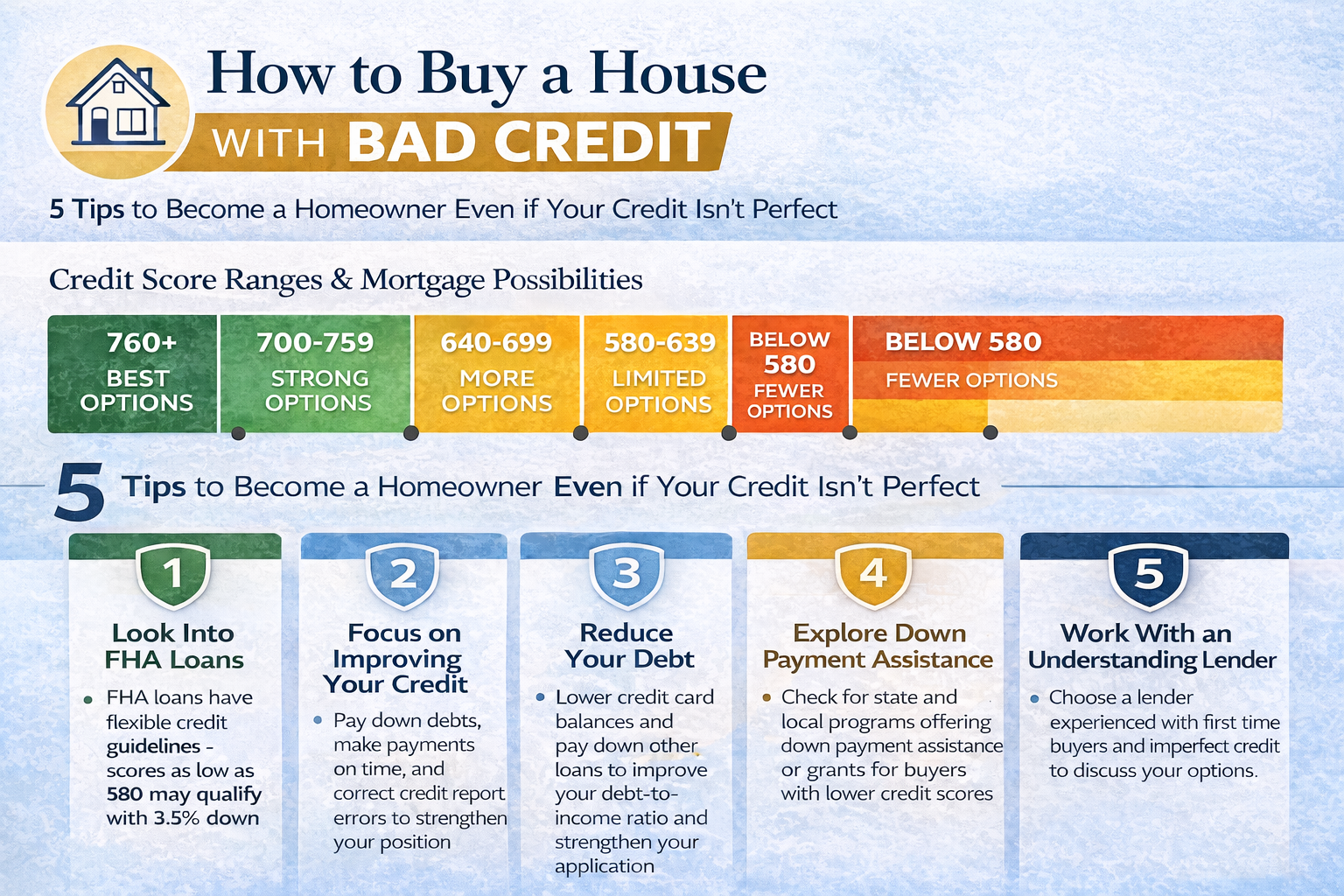

What Lenders Consider Bad Credit

In the mortgage world, credit scores generally fall into several ranges.

Typical credit score ranges include

• 760 and above for the best interest rates

• 700 to 759 for strong loan options

• 640 to 699 where many programs are still available

• 580 to 639 where some loan programs may still work

• Below 580 where options become more limited

Even if your score is in the lower ranges, there are still loan programs designed to help buyers become homeowners.

Visual Idea: Credit score range chart showing which mortgage options may be available at each level.

1. Look Into FHA Loans

One of the most common options for buyers with lower credit scores is an FHA loan.

FHA loans are designed to make homeownership more accessible and often have more flexible credit requirements than conventional loans.

Key features of FHA loans include

• Credit scores as low as 580 may qualify with 3.5 percent down

• Lower credit scores may still qualify with a larger down payment

• More flexible guidelines for past credit challenges

Because of this flexibility, FHA loans are often a starting point for many first time buyers.

Visual Idea: Comparison graphic between FHA and conventional loan credit requirements.

2. Focus on Improving Your Credit Before Applying

Even small improvements in your credit score can make a meaningful difference in your mortgage approval and interest rate.

Many buyers spend a few months strengthening their credit before applying for a loan.

Common strategies include

• Paying down credit card balances

• Making all payments on time

• Avoiding opening new credit accounts

• Disputing errors on your credit report

• Keeping credit utilization low

Raising your score even 20 to 40 points can sometimes lower your monthly payment and increase loan options.

Visual Idea: Simple infographic showing five steps to improve credit before buying a home.

3. Reduce Your Debt to Improve Your Approval Chances

Lenders look at something called your debt to income ratio, which compares your monthly debt payments to your income.

High credit card balances or large monthly debt payments can sometimes make loan approval more difficult.

Reducing debt before applying can improve your financial profile and strengthen your application.

Examples include

• Paying down credit card balances

• Avoiding new loans or financing

• Consolidating certain debts if appropriate

Lower debt levels can increase the amount you qualify to borrow.

Visual Idea: Graphic showing how debt to income ratio affects mortgage approval.

4. Explore Down Payment Assistance Programs

Many first time buyers with lower credit scores also benefit from down payment assistance programs.

These programs may offer

• Grants that do not need to be repaid

• Forgivable loans

• Assistance with closing costs

• First time buyer programs through state or local organizations

These programs can reduce the financial pressure of coming up with large upfront costs while you work toward homeownership.

Visual Idea: Chart showing common types of down payment assistance programs.

5. Work With a Lender Who Specializes in First Time Buyers

Not all lenders approach credit situations the same way.

Some lenders specialize in working with first time buyers and borrowers who are improving their credit.

A good lender can help you

• Review your credit report

• Identify areas that can improve your score

• Determine when you may qualify for a mortgage

• Explore loan programs designed for your situation

Sometimes buyers are closer to qualifying than they realize.

Key Takeaways

Buying a home with bad credit may take a little extra preparation, but it is possible in many situations.

Important things to remember

• Credit scores below perfect do not automatically prevent homeownership

• FHA loans often provide more flexible credit requirements

• Improving your credit even slightly can strengthen your application

• Reducing debt helps improve loan approval chances

• Down payment assistance programs may help reduce upfront costs

With the right strategy and preparation, many buyers successfully purchase homes while continuing to improve their credit.

Want to Know If You Could Qualify for a Home?

If you are thinking about buying a home but are unsure whether your credit is strong enough, the best place to start is with a conversation.

During a consultation, we can discuss

• Your current financial situation

• Loan options that may be available to you

• Steps that could improve your approval chances

• A timeline for when buying a home may be realistic

🏡 Schedule a Home Buying Consultation

If you want help creating a plan to buy your first home, schedule a consultation and we can walk through your options together.